Prime Minister of Malaysia. View Taxation_Question_2020_Marchpdf from ART 3240 at University Malaysia Sarawak.

Managing Your Personal Taxes 2021 22 A Canadian Perspective Ey Canada

Businesses Income loss Amount RM Business 1 Malaysia Statutory income 190270 Business 2 Malaysia Adjusted loss 76930.

. The accounts are closed on 31 December each year. Is this statement true or false. Question and Answer of Finance and Taxation.

Refer to the Section 7 1 c Individual is in Malaysia. Input Tax and Output Tax 9. The following tax rates are to be used in answering the questions.

Overview of Malaysian Taxation Q1 Double Taxation Agreement does not form part of the subsidiary legislation. Income tax rates Resident individuals Chargeable income Rate Cumulative tax RM RM RM First 5000 0 5000 00 Next 15000 5001 20000 2 300 Next 15000 20001 35000 6 1200 Next 15000 35001 50000 11 2850. The list of institutions that are allowed to accept deposits to perform foreign currencies trading and to do remittance can be referred to our official Bank Negara Malaysias website.

Malaysian Institute of Accountants Established under the Accountants Act 1967 Institut Akauntan. He passed away in Bangkok on 30 September 2018 intestate. On first RM500000 18 Subsequent Balance 24 c Resident individuals Chargeable Income Rate Cumulative Tax RM RM First 2500 0 0.

Section A ALL 15 questions are compulsory and MUST be attempted Please use the grid provided on page two of the Candidate Answer Booklet to record your answers to each multiple choice question. Q3 The Government can introduce changes to the tax laws at any time to regulate and control the economy. In the basis year for a period amounting 90 days or more.

Partners are not liable to tax on their share of income from Limited Liability Partnership whether distributed or not. Capital Goods Adjust 12. TAX RATES AND ALLOWANCES The following tax rates allowances and values are to be used in answering the questions.

User Manual User Manual About Us About Us. Tax computation for the year of assessment 2016. SET 1 ANSWER FOR EXAM SEPTEMBER 2016 MIAQE TAXATION.

To view PDFs of past exam papers for Malaysia please select from the list below. None of the above. You must NOT write in your answer booklet until instructed by the supervisor.

This question paper must not be removed from the examination hall. During reading and planning time only the question paper may be annotated. Income tax rates Resident individuals Chargeable income Rate Cumulative tax RM RM RM First 5000 0 5000 0 0 Next 15000 5001 20000 1 150 Next 15000 20001 35000 5 900 Next 15000 35001 50000 10 2 Next 20000 50001 70000 16 5 Next.

Finance questions and answers. RM450000 RM50000 RM450000 x 1090 RM500 Tutorial note. National Recovery Plan NCR.

Question 3 a An individual resident in Malaysia is taxed on any income accruing in derived from or received in Malaysia from outside Malaysia Sec. Note Add Ded - Business income RM000 RM000 RM000. TAX RATES AND ALLOWANCES The following tax rates allowances and values are to be used in answering the questions.

The company has imported a product name Fresh Mango Peach Flavour valued at RM845000 on 1 March 2022. TX-MYS paper past exams. 7 April 2018 iii.

The following tax rates are to be used in answering the questions. On first RM500000 19 Subsequent Balance 24 c Resident individuals Income tax rate for resident individuals Chargeable income Rate Cumulative tax. 4B Life insurance premiums and contributions to approved funds RM4000 RM3800 RM7800 maximum RM6 Medical and education insurance premiums for himself and his children RM1900 RM1500 RM3400.

Do NOT record any of your answers on the question paper. Taxation Paper F6 MYS Malaysia Specimen Exam applicable from. As per Income Tax Act 1961 income tax is charged on the income of at a rates which are prescribed by the Finance Act of relevant assessment year.

16010 Cost of sales 3 Less. Or ii if no compliance officer is appointed any one or all of the partners. At least 4 out of the 5 immediate preceding years of assessmentheshe was either resident in Malaysia or in Malaysia for 90 days or more.

The goods will arrive in a normal box which cannot be reuse. 3 ITA However foreign sourced income is tax exempt - Para 28 Sch 6 Sec 132c -p112 Gross income in respect of gains or profits from an employment for any period during which the employee performs outside Malaysia duties incidental to the. For the year ended 31 December 2018 the trading results were as follows.

As the technical services was performed in Malaysia it is classified as section 4A i class of income and would be subject to withholding tax under section 109B Withholding tax due. Bahasa Melayu BM Register Login. Income tax rates a Companies 24 b Small companies Chargeable income.

A Guide to Malaysian Taxation Fifth Edition REVIEW QUESTIONS CHAPTER 1. None of the above. Malaysian Taxation Question 1 A.

Payment made to Beseri Bhd This is a payment to Malaysian resident company so withholding tax is not. Malaysia and one in Thailand. Returns Payments Refunds Power to Raise Assessments Disregard Arrangements Etc 10.

As the business is growing and expanding Seri and Bayu are currently agreed to convert their partnership business to another form of. A tax deduction is not permitted in respect of the 10 late payment penalty of RM5000. Income tax rates a Companies 24 b Small companies Chargeable income.

100 Questions and Answers book tackles the practical administrative and operational questions of GST using a question-and-answer format. The Income Tax Act came into force all over India except. Seribayu Enterprise is a partnership business owned by Seri and Bayu engaged in supplying fresh flowers to customers in Kuala Lumpur and Selangor.

Accounting questions and answers Royal Malaysian Customs Department taxation Fresh Drinks Sdn Bhd The company is a private limited company incorporated on 24 February 2005. ANSWER 1 Merci Engineering Sdn. Do not write out the answers to the MCQs on the lined pages of the answer booklet.

Any pointers to the general public on how to detect an illegal scheme. 75000 x 10 RM7500 Due date. Q2 Define a person under the Income Tax Act 1967.

Citizen or permanent resident of Malaysia and ordinarily resides in Malaysia. To practice TX MYS exams in the CBE environment you can access the June September and December 2019 sample questions and answers.

What Is Difference Between Nri And Nre Account Nri Saving And Investment Tips Savings And Investment Accounting Investment Tips

Introduction To Income Tax Computation Acca Taxation Tx Uk Exam Fa2019 Youtube

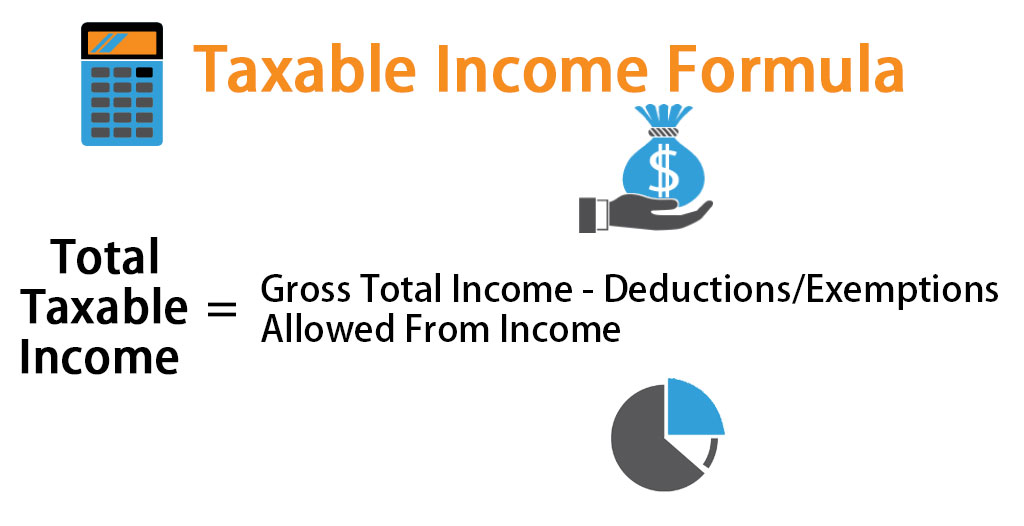

Taxable Income Formula Calculator Examples With Excel Template

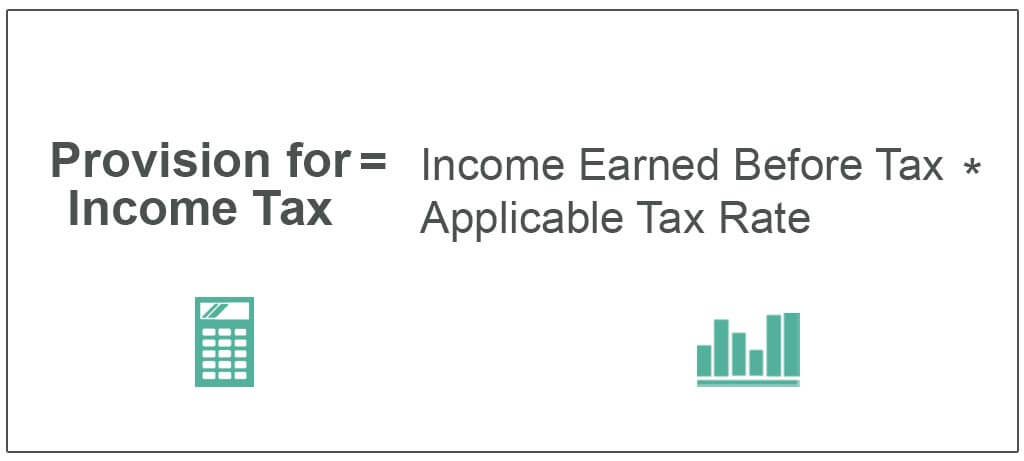

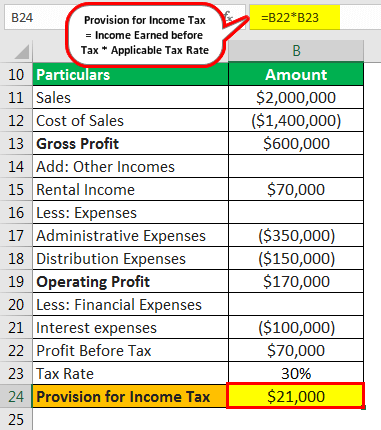

Provision For Income Tax Definition Formula Calculation Examples

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

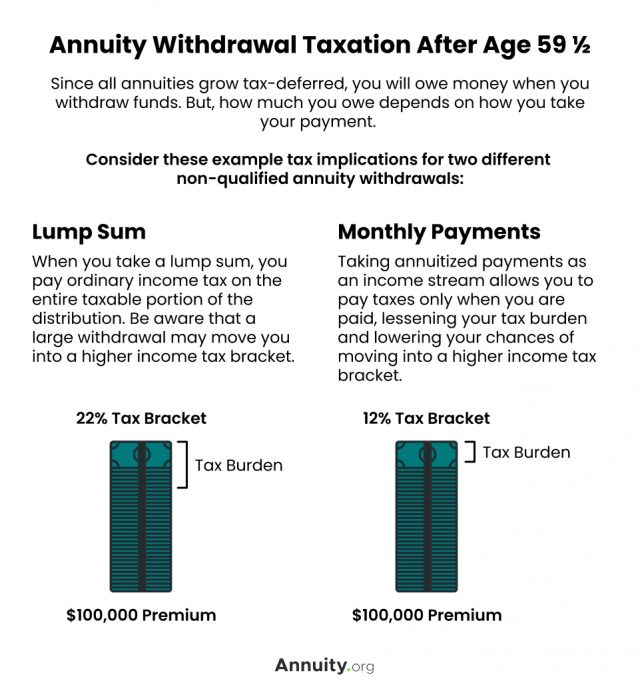

Annuity Taxation How Various Annuities Are Taxed

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

Interview Not Enough Americans Pay Income Tax Should They

Advantages And Disadvantages Of Gst In Malaysia Financial Aid For College Tax Software Mortgage Interest

Taxation Definition

Gold Pound Symbol British Pound Symbol Isolated On White Paid Affiliate Sponsored Symb Simbolo De Libra Como Economizar Dinheiro Graficos Financeiros

Is Aadhaar Card Mandatory For Nri Cards Finance City Office

Double Taxation Oveview Categories How To Avoid

Pin On Finance And Money

:max_bytes(150000):strip_icc()/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

How To Calculate Your Income Tax Step By Step Guide For Income Tax Calculation Youtube

Provision For Income Tax Definition Formula Calculation Examples

Can You Deposit Indian Rupees To Nre Account Savings Investment Tips Savings And Investment Accounting Investment Tips

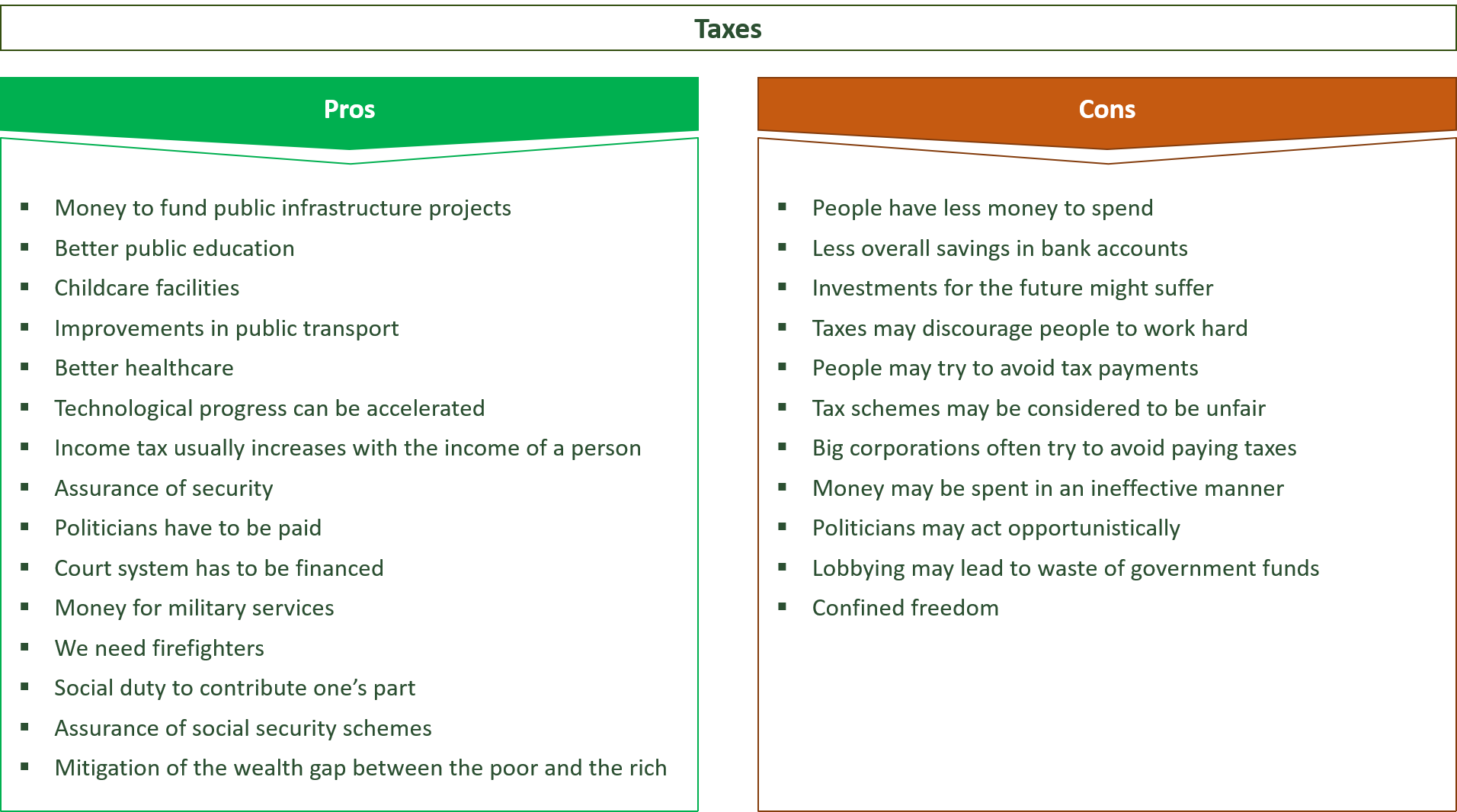

29 Crucial Pros Cons Of Taxes E C